Rent or Own?

For Millennials and First-Time Home Buyers, there is always the question of Rent or Own? Renting and owning a house each have their own advantages and disadvantages. When considering whether to rent or own a house, there are several factors to take into account, especially for millennials. Know that you can always contact us here and our lenders will take the time to listen and help you sort through your options. In the meantime, here are some key points to consider:

For Millennials and First-Time Home Buyers, there is always the question of Rent or Own? Renting and owning a house each have their own advantages and disadvantages. When considering whether to rent or own a house, there are several factors to take into account, especially for millennials. Know that you can always contact us here and our lenders will take the time to listen and help you sort through your options. In the meantime, here are some key points to consider:

Renting a House:

Advantages:

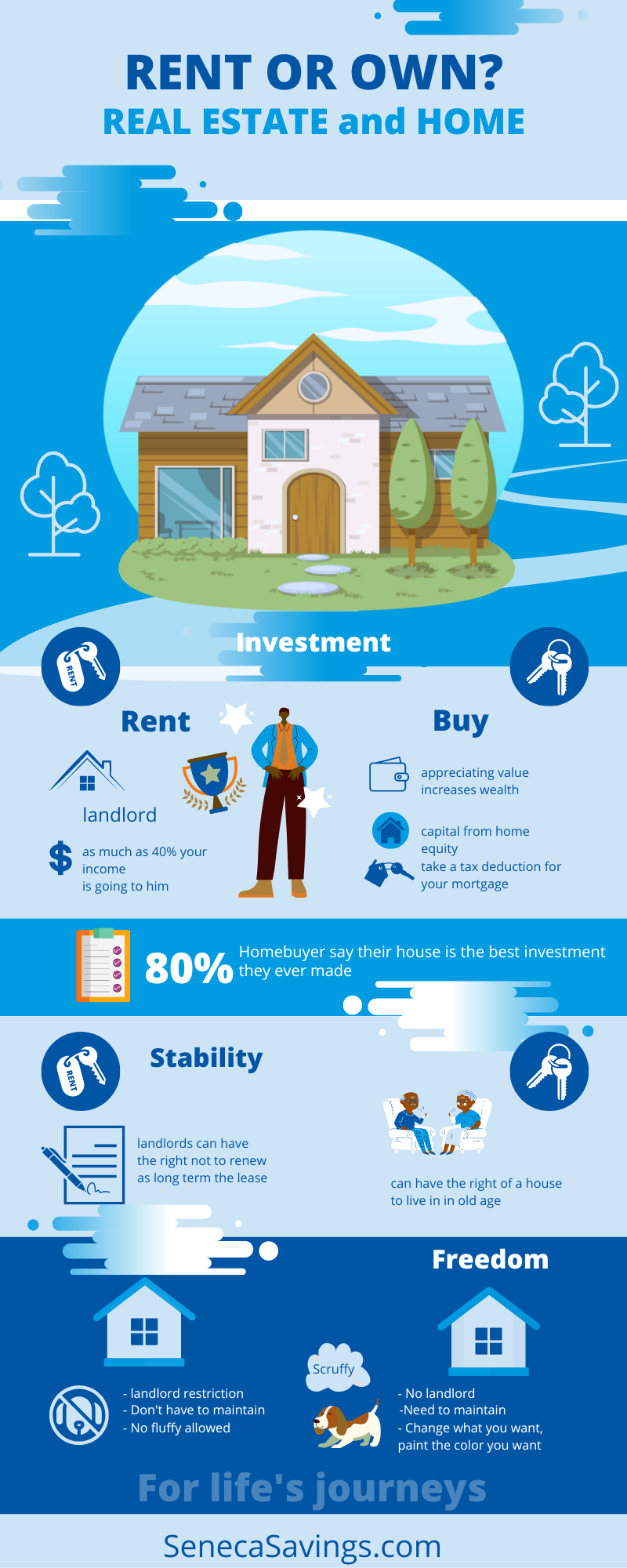

1. Flexibility: Renting provides more flexibility in terms of mobility. Millennials often value the ability to easily move for career opportunities or personal reasons without being tied down to a particular location.

2. Lower upfront costs: Renting typically requires less upfront costs compared to buying a house. You may only need to pay a security deposit and first month’s rent, making it more affordable in the short term.

3. Maintenance responsibility: Generally, the landlord is responsible for property maintenance and repairs, which can save you time, effort, and money.

Disadvantages:

1. Lack of equity: Renting means you are not building equity in a property. You don’t benefit from potential appreciation in the housing market, and your monthly payments are not contributing to your own asset.

2. Limited control: As a renter, you have limited control over the property. You may face restrictions on making modifications or personalizing the space according to your preferences.

3. Rent fluctuations: Rent prices are subject to market fluctuations and may increase over time. This lack of predictability can make long-term financial planning challenging.

Owning a House:

Advantages:

1. Building equity: Buying a house allows you to build equity over time as you make mortgage payments. This can potentially provide a financial asset and a source of wealth.

2. Stability and roots: Owning a home can offer a sense of stability and roots in a community. It provides the opportunity to establish long-term connections and create a place that truly feels like your own.

3. Potential tax benefits: Homeownership may come with tax advantages, such as deductions for mortgage interest and property taxes, which can help reduce your overall tax liability.

Disadvantages:

1. Financial commitment: Owning a house requires a significant financial commitment. You’ll need to cover a down payment, closing costs, property taxes, insurance, and ongoing maintenance expenses.

2. Limited mobility: Buying a house ties you to a specific location, which may limit your ability to move quickly for job opportunities or other lifestyle changes.

3. Maintenance and responsibilities: As a homeowner, you are responsible for property maintenance and repairs. These costs can add up over time, and you’ll need to invest time and money into maintaining your home.

When deciding whether to rent or own a house, it’s essential to consider your financial situation, long-term plans, lifestyle preferences, and personal goals. Here’s another helpful article that lays out the different considerations a first time home buyer may wish to consider. Factors such as your career trajectory, housing market conditions, monthly budget, and desired level of control over your living space should also be taken into account. It can be helpful to evaluate the costs and benefits of each option based on your specific circumstances and prioritize what aligns with your priorities and values.

Consult with your experienced banker to understand your financial situation and explore mortgage options. Working with a banker can provide insights into affordability, down payment requirements, and potential financing strategies. Building up enough for a down payment requires diligent saving and budgeting. Millennials in particular, can consider strategies like creating a separate savings account dedicated to the down payment, cutting unnecessary expenses, and exploring potential assistance programs for first-time homebuyers.

It’s important to consider individual circumstances and goals when deciding between renting and owning a house. Factors such as career trajectory, housing market conditions, monthly budget, and desired level of control over the living space should all be taken into account. Evaluating the costs and benefits of each option and seeking advice from professionals like bankers can help millennials and first-time home buyers make informed decisions that align with their financial goals and aspirations.

Wherever you’re at in your journey, Seneca Savings is there for you and ready to help!

Member FDIC Equal Housing Lender